Chase Minimum Payment Due Vs Statement Balance

adminse

Apr 05, 2025 · 8 min read

Table of Contents

Chase Minimum Payment Due vs. Statement Balance: Understanding the Difference and Choosing Your Strategy

What's the crucial difference between paying the Chase minimum payment due versus the statement balance, and how does this impact your financial well-being?

Understanding the nuances of minimum payments versus paying your statement balance in full is key to avoiding high interest charges and building a strong credit profile.

Editor’s Note: This article on Chase minimum payment due vs. statement balance was published today. It provides crucial insights into managing credit card debt effectively.

Why Understanding Chase Minimum Payment Due vs. Statement Balance Matters

Navigating the world of credit cards requires a clear understanding of payment options. Many Chase cardholders often confuse the minimum payment due with the statement balance, leading to potentially significant financial consequences. Understanding the difference is crucial for managing debt effectively, avoiding high interest charges, and protecting your credit score. This knowledge empowers you to make informed financial decisions, ultimately contributing to long-term financial health. The implications extend beyond individual financial management, impacting broader economic stability and responsible credit use.

Overview of the Article

This article comprehensively explores the distinction between the Chase minimum payment due and the statement balance. We'll delve into the calculation of minimum payments, the impact of only paying the minimum on interest accrual, and the advantages of paying your statement balance in full. We will also explore strategies for managing debt effectively and improving your credit score. Finally, we will address frequently asked questions and offer practical tips to optimize your Chase credit card repayment strategy.

Research and Effort Behind the Insights

The information presented in this article is based on extensive research of Chase's credit card terms and conditions, analysis of industry best practices in credit card management, and examination of consumer financial reports. We've consulted reputable financial sources to ensure accuracy and provide readers with actionable advice based on proven methodologies.

Key Takeaways

| Key Concept | Explanation |

|---|---|

| Minimum Payment Due | The smallest amount you can pay to avoid late fees and remain in good standing with your credit card issuer. |

| Statement Balance | The total amount you owe on your credit card as of the statement closing date. |

| Interest Accrual | Interest charges accumulate on outstanding balances, significantly impacting your total repayment amount. |

| Credit Score Impact | Consistent minimum payments can negatively impact your credit score, while full payments improve it. |

| Debt Management Strategies | Several strategies exist to manage credit card debt effectively, including the debt snowball and avalanche methods. |

Smooth Transition to Core Discussion

Let's delve deeper into the core differences between the minimum payment due and the statement balance, exploring their impact on your financial situation and offering strategies for optimal debt management.

Exploring the Key Aspects of Chase Credit Card Payments

-

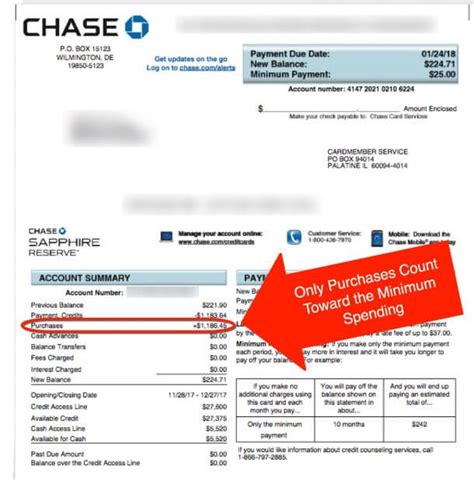

Understanding the Minimum Payment: The minimum payment due is calculated as a percentage of your statement balance (usually 1-3%, but it can vary). It's the bare minimum required to avoid late fees and negative impacts on your credit report. However, paying only the minimum leaves a substantial balance subject to high interest charges.

-

The Statement Balance: This is the total amount you owe, including purchases, fees, and interest accrued since your last statement. Paying your statement balance in full each month eliminates interest charges entirely.

-

Interest Accrual and APR: The Annual Percentage Rate (APR) determines the interest rate applied to your outstanding balance. The higher your APR, the faster interest charges accrue. Paying only the minimum drastically increases the amount you ultimately pay over time.

-

Impact on Credit Score: Consistently paying only the minimum payment negatively impacts your credit utilization ratio (the percentage of your available credit that you're using). A high credit utilization ratio lowers your credit score, potentially affecting your ability to obtain loans or favorable interest rates in the future. Paying your statement balance in full demonstrates responsible credit management, contributing to a better credit score.

-

Debt Management Strategies: If you find yourself consistently paying only the minimum, consider debt management strategies like the debt snowball (paying off the smallest debt first for motivation) or the debt avalanche (paying off the debt with the highest interest rate first for cost savings). These methods help you systematically reduce your debt and regain financial control.

-

Avoiding Late Fees: Always pay at least the minimum payment by the due date to avoid late payment fees, which further increase your debt burden.

Closing Insights

The choice between paying the Chase minimum payment due and the statement balance has significant implications for your financial health. While paying the minimum might seem convenient in the short term, it prolongs debt repayment and leads to higher overall costs due to accumulated interest. Prioritizing the payment of your statement balance in full, or employing effective debt management strategies, demonstrates responsible financial behavior, improves your credit score, and saves you substantial money in the long run. Remember to always check your credit card statement carefully and budget accordingly to avoid unnecessary debt.

Exploring the Connection Between Credit Utilization and Paying Only the Minimum

High credit utilization, often a consequence of consistently paying only the minimum, significantly impacts your credit score. Lenders view a high credit utilization ratio as a sign of potential financial instability. This is because a large portion of your available credit being used suggests that you may struggle to manage your finances. The effect on your credit score can make it harder to secure loans, mortgages, or even rent an apartment in the future. Conversely, maintaining a low credit utilization ratio (ideally below 30%) signals responsible credit management, positively affecting your creditworthiness.

Further Analysis of Interest Accrual

Interest accrual compounds over time. Even a seemingly small difference in your APR can result in a substantial increase in the total amount paid over the life of the debt. For instance, paying only the minimum on a $5,000 balance with a 20% APR for a year could cost hundreds of dollars more in interest compared to paying the statement balance in full. Understanding this compounding effect highlights the long-term financial benefits of paying off your credit card debt as quickly as possible. This understanding is crucial for making informed decisions about debt management.

FAQ Section

-

Q: What happens if I only pay the minimum payment on my Chase credit card?

A: You will avoid late fees, but you'll accumulate interest on the remaining balance, significantly increasing the total cost of your purchases over time. It will also negatively impact your credit utilization ratio.

-

Q: How is the minimum payment calculated?

A: The minimum payment is typically a percentage (often 1-3%) of your statement balance, but it can vary depending on your card agreement. Check your statement for the exact calculation.

-

Q: Can I negotiate a lower minimum payment?

A: It's unlikely Chase will negotiate a lower minimum payment. However, you can explore options like balance transfers to lower your interest rate or consider debt management plans.

-

Q: What is the best way to manage my credit card debt?

A: Prioritize paying your statement balance in full each month. If that's not possible, develop a debt management strategy (like the snowball or avalanche method) to systematically pay down your debt.

-

Q: Will paying only the minimum affect my credit score?

A: Yes. It increases your credit utilization ratio, which negatively impacts your credit score. Aim to keep your credit utilization below 30%.

-

Q: What should I do if I can't afford to pay my statement balance in full?

A: Contact Chase immediately to discuss options, such as a hardship program or debt management plan. Avoid ignoring the debt, as this will further harm your credit score.

Practical Tips

-

Budget Carefully: Track your spending and create a budget to ensure you can afford to pay your statement balance in full each month.

-

Automate Payments: Set up automatic payments to avoid missing deadlines and late fees.

-

Pay More Than the Minimum: Whenever possible, pay more than the minimum payment to reduce your balance faster and lower overall interest charges.

-

Monitor Your Credit Report: Regularly check your credit report for accuracy and identify any potential issues.

-

Explore Debt Consolidation: Consider consolidating high-interest debts onto a lower-interest loan or credit card.

-

Seek Professional Help: If you're struggling to manage your debt, consult a financial advisor for personalized guidance.

-

Avoid New Debt: Refrain from taking on new debt until you've significantly reduced your existing debt.

-

Understand Your APR: Know your APR and how it impacts your interest charges.

Final Conclusion

Understanding the difference between Chase minimum payment due and the statement balance is crucial for responsible credit card management. Paying only the minimum may seem convenient, but it significantly increases the overall cost of borrowing. Prioritizing full payment of your statement balance each month, coupled with sound budgeting and debt management strategies, safeguards your financial well-being, protects your credit score, and ultimately helps you achieve long-term financial success. Remember that proactive financial management leads to greater stability and peace of mind. Stay informed, stay responsible, and take control of your financial future.

Latest Posts

Latest Posts

-

Cara Mengatur Money Management

Apr 06, 2025

-

Cara Kerja Fund Manager

Apr 06, 2025

-

Cara Money Management

Apr 06, 2025

-

Money Management Group Activities

Apr 06, 2025

-

How To Become A Money Manager

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about Chase Minimum Payment Due Vs Statement Balance . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.