Minimum Payment On 600 Credit Card

adminse

Apr 05, 2025 · 9 min read

Table of Contents

Decoding the Minimum Payment on a 600 Credit Score Card: Discoveries and Insights

What are the implications of only making minimum payments on a credit card with a 600 credit score?

Understanding your minimum payment is crucial for responsible credit management, regardless of your credit score. Ignoring this can lead to severe financial consequences.

Editor’s Note: Understanding minimum payments on credit cards with a 600 credit score has been published today.

Why Minimum Payments Matter (Especially with a 600 Credit Score)

A credit score of 600 is considered fair, placing you in a somewhat precarious position regarding credit access. Lenders view this score as moderately risky, often resulting in higher interest rates and stricter lending terms. Understanding and managing your minimum payments on credit cards is paramount in this scenario. Failing to do so can significantly impact your financial health in several ways:

-

Increased Debt: The most immediate consequence of only paying the minimum is the slow accumulation of debt. A significant portion of your payment goes towards interest, leaving a small amount to reduce your principal balance. This snowball effect can trap you in a cycle of debt for years.

-

Higher Interest Charges: Credit cards typically have high Annual Percentage Rates (APRs). Paying only the minimum means you're paying more interest over time, which dramatically increases the total cost of your purchases. This is especially impactful for those with a 600 credit score, as they often face higher APRs compared to those with better credit.

-

Damaged Credit Score: Consistent minimum payments, particularly when coupled with missed payments or exceeding your credit limit, can negatively affect your credit score. This makes it harder to secure loans, rent an apartment, or even get approved for some jobs. The impact is more significant given your existing 600 score – a further drop can severely limit your financial options.

-

Late Payment Fees: Even a single missed payment, or a payment that is less than the minimum, can lead to late payment fees. These fees add up quickly and can further hinder your progress in paying off your debt. This is particularly damaging with a fair credit score, increasing the risk of further credit score decline.

Overview of This Article

This article delves into the intricacies of minimum payments on credit cards, specifically focusing on the implications for individuals with a 600 credit score. We will explore the calculation of minimum payments, the impact of various factors, strategies for effective debt management, and common pitfalls to avoid. Readers will gain a comprehensive understanding of how minimum payments affect their financial well-being and actionable steps to improve their credit situation.

Research and Effort Behind the Insights

This article is based on extensive research, including analysis of credit card agreements, industry reports from reputable sources like Experian, Equifax, and TransUnion, and insights from financial experts. The information provided is designed to be accurate, up-to-date, and relevant to the current financial landscape.

Key Takeaways

| Key Point | Explanation |

|---|---|

| Minimum Payment Calculation | Varies by issuer; often a percentage of the balance or a fixed minimum, whichever is greater. |

| Impact of High APR on Minimum Payments | Significantly increases the time it takes to pay off debt and the total interest paid. |

| Credit Score Implications | Consistent minimum payments can damage credit scores, especially with already fair credit. |

| Strategies for Debt Reduction | Debt consolidation, balance transfers, and budgeting can help manage debt more effectively. |

| Importance of Financial Literacy | Understanding credit card agreements and financial principles is critical for responsible credit card usage. |

Smooth Transition to Core Discussion

Now, let's delve deeper into the specifics of minimum payments on credit cards with a 600 credit score, starting with how these minimums are calculated.

Exploring the Key Aspects of Minimum Payments on a 600 Credit Score Card

-

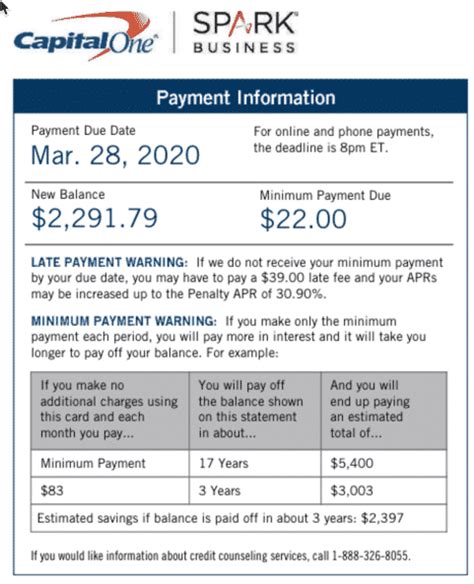

Minimum Payment Calculation: The minimum payment isn't a fixed amount. It's typically calculated as a percentage of your outstanding balance (often 1-3%), or a fixed minimum dollar amount, whichever is higher. Check your credit card statement for the exact calculation used by your issuer.

-

Impact of APR: The Annual Percentage Rate (APR) directly affects how much interest accrues on your balance. With a 600 credit score, you're likely facing a higher APR than someone with excellent credit. This means a larger portion of your minimum payment goes towards interest, prolonging debt repayment.

-

Debt Snowball Effect: Only paying the minimum creates a vicious cycle. The interest keeps accumulating, making it feel like you’re making little to no progress towards paying off the principal balance. This “debt snowball” can quickly overwhelm even those with diligent repayment habits.

-

Credit Reporting and Score: Payment history is a significant factor in your credit score. Consistently paying only the minimum, though technically not a missed payment, doesn’t portray responsible credit management. Lenders see this as a potential risk.

-

Missed Payments and Fees: Even a single missed minimum payment negatively impacts your credit score, attracting late payment fees, which further increase your debt. For someone with a 600 credit score, this is exceptionally detrimental.

-

Available Debt Management Strategies: Several strategies can help you manage your debt more effectively. These include debt consolidation (combining multiple debts into one loan with potentially a lower interest rate), balance transfers (moving your balance to a card with a lower APR), and creating a comprehensive budget to control spending.

Closing Insights

Paying only the minimum payment on a credit card, especially with a 600 credit score, is a risky strategy that can lead to long-term financial difficulties. The high interest rates associated with fair credit amplify the negative consequences of this approach. Understanding the intricacies of minimum payment calculations, the impact of APRs, and the potential damage to your credit score is vital for making informed financial decisions. Exploring debt management strategies and prioritizing responsible credit card usage are crucial steps towards improving your financial health.

Exploring the Connection Between Financial Literacy and Minimum Payments

Financial literacy plays a crucial role in understanding and managing minimum payments. Individuals lacking financial knowledge might underestimate the long-term costs of only making minimum payments. Understanding concepts like APR, compound interest, and credit scoring is essential for making responsible financial decisions. This knowledge empowers individuals to avoid the debt traps associated with insufficient minimum payments. Real-world examples abound – individuals unaware of the snowball effect of minimum payments often find themselves in overwhelming debt, impacting their credit scores and future financial opportunities.

Further Analysis of the Impact of High APRs

High APRs significantly amplify the negative impacts of only making minimum payments. A higher APR means a larger portion of your payment goes towards interest, leaving less to reduce the principal balance. This leads to a longer repayment period and substantially increased total interest paid over the life of the debt. For someone with a 600 credit score facing potentially higher APRs, this effect is magnified, further delaying debt repayment and potentially causing long-term financial difficulties. Data from consumer finance reports consistently demonstrate the direct correlation between high APRs, minimum payment strategies, and increased debt burden.

FAQ Section

-

Q: What happens if I only make minimum payments on my credit card? A: You’ll pay significantly more in interest over time, extending the repayment period and increasing the total cost of your purchases. It can also negatively impact your credit score.

-

Q: How is the minimum payment calculated? A: It’s usually a percentage of your outstanding balance (often 1-3%) or a fixed minimum dollar amount, whichever is greater. Check your credit card statement for specifics.

-

Q: Can I improve my credit score if I'm consistently making minimum payments? A: While not damaging your credit as much as missing payments, consistently making only the minimum won’t improve your credit score. To improve your score, you need to pay more than the minimum and actively manage your credit utilization.

-

Q: What are the consequences of missing minimum payments? A: Missed payments severely damage your credit score, leading to late fees and potential collection actions. It can also make it difficult to obtain future credit.

-

Q: How can I get out of credit card debt? A: Consider debt consolidation, balance transfers, or creating a detailed budget to reduce spending and accelerate debt repayment. Seek advice from a financial advisor if needed.

-

Q: Is there a difference between minimum payment on a secured vs. unsecured credit card? A: While the calculation method may be similar, secured cards (backed by a security deposit) may offer slightly lower APRs, but this doesn’t negate the negative impacts of only paying the minimum.

Practical Tips

-

Track your spending: Monitor your credit card usage diligently to avoid accumulating excessive debt.

-

Create a budget: Allocate funds specifically for credit card payments to ensure timely and sufficient payments.

-

Pay more than the minimum: Even a small increase in your payment can significantly reduce the total interest paid and shorten your repayment timeline.

-

Consider a balance transfer: Transfer your balance to a card with a lower APR to reduce the interest you pay.

-

Explore debt consolidation: Combine your debts into a single loan with potentially a lower interest rate and a more manageable monthly payment.

-

Negotiate with your creditor: If facing financial hardship, contact your credit card issuer to discuss potential payment arrangements.

-

Seek professional help: Consult a financial advisor or credit counselor for personalized advice and debt management strategies.

-

Improve your credit score: Focus on building good credit habits to qualify for lower interest rates in the future.

Final Conclusion

Understanding the implications of minimum payments on a credit card with a 600 credit score is crucial for financial well-being. While making the minimum payment avoids immediate penalties, it prolongs debt repayment, increases overall costs, and hinders credit score improvement. Active management of credit, incorporating responsible spending habits, and exploring debt management strategies are essential for navigating the complexities of credit card debt and building a solid financial foundation. Proactive steps today can lead to a healthier financial future tomorrow.

Latest Posts

Latest Posts

-

What Does Nfc Mobile Payment Mean

Apr 06, 2025

-

What Does Nfc Mobile Payment Stand For

Apr 06, 2025

-

What Is Nfc Mobile Pay

Apr 06, 2025

-

What Is Nfc Mobile Payments

Apr 06, 2025

-

What If Nfc Mobile Payments

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about Minimum Payment On 600 Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.