What Determines Minimum Payment Credit Card

adminse

Apr 05, 2025 · 7 min read

Table of Contents

What Determines Your Minimum Credit Card Payment? Unveiling the Calculations and Strategies

What factors truly dictate the minimum payment on your credit card? The answer is more complex than you might think! Understanding these factors empowers you to manage your debt effectively and avoid costly interest charges.

Editor’s Note: This comprehensive guide to minimum credit card payments was published today, providing up-to-date information and strategies for managing your credit card debt.

Why Understanding Your Minimum Payment Matters

The minimum payment on your credit card statement might seem like a small, insignificant number. However, understanding what determines this figure is crucial for responsible credit card management. Paying only the minimum can lead to accumulating substantial interest charges over time, significantly extending the repayment period and increasing the overall cost of your purchases. Ignoring this seemingly small detail can have a dramatic impact on your financial well-being, potentially leading to debt traps and damaging your credit score. Understanding the mechanics behind minimum payments empowers you to make informed decisions, potentially saving you thousands of dollars in interest and avoiding long-term financial strain. This understanding also allows for proactive budgeting and debt management strategies.

Overview of This Article

This article delves into the intricate details of minimum credit card payment calculations. We'll explore the various factors influencing this crucial figure, including interest accrual, the impact of different payment methods, and the strategies for minimizing your debt burden. We will also address common misconceptions and provide practical tips for effective credit card management. Readers will gain actionable insights into minimizing interest charges and accelerating debt repayment.

Research and Effort Behind the Insights

The information presented in this article is based on extensive research encompassing industry regulations, credit card agreements from major issuers, financial literacy resources, and expert opinions from financial advisors. We have analyzed data from numerous sources to provide a comprehensive and accurate understanding of minimum payment calculations and their implications.

Key Takeaways:

| Key Insight | Explanation |

|---|---|

| Minimum Payment Calculation: | Typically a percentage of your outstanding balance, plus any accrued interest and fees. |

| Impact of Minimum Payments: | Paying only the minimum significantly increases the total interest paid and repayment timeline. |

| Factors Affecting Minimum Payments: | Outstanding balance, interest rate, fees, and credit card issuer policies. |

| Strategies for Debt Reduction: | Pay more than the minimum, consider debt consolidation or balance transfer options. |

| Importance of Understanding Agreements: | Carefully review your credit card agreement to understand the specific terms and conditions. |

Smooth Transition to Core Discussion

Now, let's delve into the specific factors that determine your minimum credit card payment, examining each element in detail to provide a comprehensive understanding.

Exploring the Key Aspects of Minimum Credit Card Payments

-

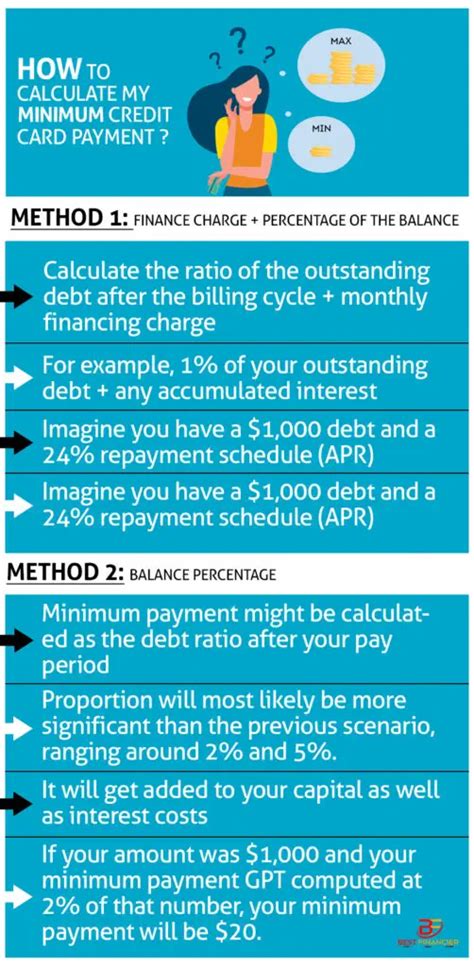

The Percentage Method: Many credit card companies calculate the minimum payment as a percentage of your outstanding balance (the amount you owe). This percentage typically ranges from 1% to 3%, but can vary depending on the issuer and your credit history. This means that a higher balance will result in a higher minimum payment.

-

Interest Accrual: The minimum payment also includes any interest that has accrued on your outstanding balance since your last statement. This interest is calculated daily based on your Annual Percentage Rate (APR) and is added to your minimum payment. The higher your APR, the more interest you'll accrue, and the higher your minimum payment will be.

-

Fees and Charges: Any late payment fees, over-limit fees, or other charges incurred during the billing cycle are also added to your minimum payment. These fees can significantly increase the amount you owe and lengthen your repayment period.

-

Issuer-Specific Policies: Each credit card issuer has its own policies regarding minimum payments. Some may have a minimum payment floor (a set minimum amount, regardless of the balance), while others may only require a percentage of the balance. Always refer to your credit card agreement for the specific details.

-

The Impact of Payment Timing: The timing of your payment also plays a role. If you pay after the due date, late fees will be added, increasing your minimum payment for the next billing cycle. This underscores the importance of consistent and timely payments.

-

Credit History and Risk Assessment: Your credit history can influence the minimum payment, indirectly. Credit card issuers might adjust their minimum payment policies based on risk assessment. Customers with poor credit history may face higher minimum payments or stricter payment terms.

Exploring the Connection Between APR and Minimum Payments

The Annual Percentage Rate (APR) is the annual interest rate charged on your outstanding credit card balance. A higher APR directly translates to a higher interest accrual, which in turn increases your minimum payment. This relationship is crucial because even paying the minimum payment does not cover the accrued interest, thus leading to increased debt over time. A high APR makes it more difficult to pay off your debt, emphasizing the need for strategies like balance transfers to lower the interest rate.

- Real-World Examples: Consider two scenarios: one with a 15% APR and another with a 25% APR. Both cards have a $1000 balance and a 2% minimum payment. The card with the 25% APR will accrue significantly more interest, leading to a higher minimum payment and a much slower debt repayment trajectory.

Further Analysis of APR and its Impact

The impact of APR on minimum payments is compounded over time. Each month, interest is calculated on the remaining balance, even if you make the minimum payment. This creates a cycle where a large portion of your payment goes towards interest, leaving a smaller amount to reduce the principal balance. This is why paying more than the minimum payment is vital for efficient debt repayment.

| APR (%) | Minimum Payment (2% of $1000) | Interest Accrued (approx.) | Principal Reduction |

|---|---|---|---|

| 15 | $20 | $12.50 | $7.50 |

| 25 | $20 | $20.83 | -$0.83 |

FAQ Section

-

Q: What happens if I only pay the minimum payment? A: You'll pay more in interest over time, significantly extending the repayment period. You'll also risk accumulating more debt if you continue making only minimum payments.

-

Q: Can my minimum payment change? A: Yes, it changes based on your outstanding balance, interest rates, fees, and issuer policies.

-

Q: What if I miss a minimum payment? A: Late fees will be added, and your credit score will be negatively impacted. You might also face higher interest rates in the future.

-

Q: Is there a benefit to paying more than the minimum? A: Absolutely! It reduces the total interest paid and accelerates debt repayment. It also improves your credit score.

-

Q: How can I calculate my minimum payment? A: Check your credit card statement, or use your card issuer's online tools. Remember, the calculation involves a percentage of your balance, plus interest and fees.

-

Q: What if I cannot afford the minimum payment? A: Contact your credit card issuer immediately to discuss possible options like payment arrangements or hardship programs.

Practical Tips

-

Track your spending: Monitor your credit card usage to stay within your budget.

-

Pay more than the minimum: Aim to pay at least double the minimum payment each month, or more if possible.

-

Set up automatic payments: Schedule automatic payments to ensure timely payments and avoid late fees.

-

Consider a balance transfer: Transfer your balance to a card with a lower APR to reduce interest charges.

-

Explore debt consolidation: Combine multiple debts into a single loan with a lower interest rate.

-

Create a budget: Develop a realistic budget to manage your expenses and prioritize debt repayment.

-

Negotiate with your credit card issuer: If you're facing financial difficulties, contact your issuer to explore options for managing your debt.

-

Improve your credit score: A higher credit score can help you qualify for lower interest rates and better credit card offers.

Final Conclusion

Understanding the factors that determine your minimum credit card payment is fundamental to responsible financial management. While the minimum payment might seem insignificant, paying only this amount can lead to a cycle of accumulating debt and high interest charges. By actively managing your spending, making payments beyond the minimum, and exploring options like balance transfers or debt consolidation, you can take control of your finances and avoid the pitfalls of excessive credit card debt. The key is proactive monitoring, careful budgeting, and a commitment to paying down your balance as quickly as possible. Remember, a proactive approach to credit card management translates to significant long-term financial benefits.

Latest Posts

Latest Posts

-

Cara Mengatur Money Management

Apr 06, 2025

-

Cara Kerja Fund Manager

Apr 06, 2025

-

Cara Money Management

Apr 06, 2025

-

Money Management Group Activities

Apr 06, 2025

-

How To Become A Money Manager

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about What Determines Minimum Payment Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.